Saudi Arabia

Quarterly Economic Report

Q1 2025

Published by

expert human analysis powered by advanced data tools.

Executive Summary

At the end of Q1 2025, Saudi Arabia’s economy remains resilient but faces mounting external headwinds. Real GDP grew 2.7% y/y, supported by sustained non-oil sector expansion (+4.2% y/y) and strong consumer spending, even as oil GDP contracted before the start of the Israel-Iran war on June 13.

The rise in GDP in Q1 this year is a moderation from Q4 2024’s 4.48% surge. This deceleration was mainly due to a -1.4% y/y contraction in oil GDP, reflecting the impact of subdued oil prices (before the eruption of the Israel-Iran war), while non-oil GDP maintained sustained growth at 4.2% y/y – though moderating from 4.7% y/y in Q4 2024. Non-oil activities now account for 53.2% of total GDP.

Non-oil activities now account for over half of GDP, driven by Vision 2030 megaprojects, tourism, and digital transformation, while the labour market showed further improvement with overall unemployment at 3.5% and unemployment among Saudis reached an unprecedented level of 6.3% at the end of Q1.

However, the fiscal position weakened: the Q1 2025 budget deficit widened to SAR 58.7 billion, as oil revenues fell 18% y/y, and spending on social programs and mega-projects remained high.

Non-oil exports surged 13.4% y/y in Q1 2025, but total exports declined 3.2% y/y as oil exports dropped sharply by 8.4% y/y, reducing oil’s share of total exports to 71.8% (from 75.9% in Q1 2024).

At the same time, imports rose 7.3% y/y, narrowing the trade surplus by March 2025. Inflation remains moderate at 2.1–2.3% (mainly driven by housing and food costs), but risks persist from elevated housing costs, potential subsidy reforms, and Red Sea shipping disruptions.

Looking ahead, GDP is projected to grow 3.6% in 2025, led by non-oil sector, but fiscal and external balances will remain sensitive to oil price volatility, global demand, and the pace of fiscal reforms. The outlook is cautiously optimistic: Vision 2030’s diversification is gaining traction, but sustaining momentum will require prudent fiscal management, accelerated private sector growth, and continued progress in non-oil exports, and job creation.

Non-oil sector growth in Q1 2025 was underpinned by dynamic consumer spending – in March 2025, consumer spending reached an all-time high of SAR 148 billion, up 17% y/y, while POS transactions rose 10% y/y and e-commerce soared 73.4% y/y (reflecting strong private consumption and retail momentum).

The labour market demonstrated further improvement. Overall unemployment fell to 3.5% in Q4 2024, from 3.7% in the previous quarter. Unemployment among Saudi nationals fell to 6.3% in Q1 2025, and female participation declined a bit to 36% in Q4 2024 from 36.2% in the previous quarter – despite this slight decline, the participation rate remains significantly higher than in previous years and reflects the ongoing progress of Saudi Arabia's labour market reforms.

Saudi Arabia’s industrial sector showed moderate but volatile growth in Q1 2025, with industrial production up 1.3% y/y in January, dipping 0.2% y/y in February due to weak oil output, and rebounded 2.0% y/y in March.

Manufacturing’s contribution in Saudi Arabia was uneven in early 2025. In January, output grew by 4.0% y/y, supported by gains in chemicals and refined petroleum products. Growth stagnated in February, rising just 0.2% y/y, as momentum in the sector softened despite continued increases in chemicals and food products.

In March, manufacturing output surged by 5.1% y/y, led by strong performances in chemicals (+14.3% y/y) and food products (+6.9% y/y). This pattern highlights both the sector’s growing importance to non-oil GDP and its vulnerability to global demand and supply chain risks.

Looking ahead, Saudi Arabia’s GDP is projected to grow 3.6% in 2025, with non-oil sectors forecast to expand by 4.5% and oil GDP by 2.7% - Saudi crude oil production is expected to average of 9.2 MMBD in FY2025.

Oil prices were expected to average $68.69/bbl in 2025 (our assumption), before the eruption of the Iran-Israel war. But with the onset with the serious military confrontation between both countries, Brent crude, the global benchmark, rose by 8% on June 13th, to $74 a barrel and the price per barrel could be around $90 if Israel hit key oil facilities in Iran, since the world would lose around 1.7m barrels per day from Iran.

The private sector remains optimistic, as reflected in a Purchasing Managers’ Index of 58.1 in March 2025. Sustaining the current trajectory will require accelerating high-impact sectors such as logistics and tourism, as well as addressing persistent labour market skill gaps to ensure the benefits of diversification are broadly shared amid ongoing global headwinds.

Looking ahead, the fiscal outlook for 2025 is challenging, with the deficit forecast to widen to 4.3% of GDP (SAR 188.77 billion) – above the government’s official projection of 2.3%. This wider gap is attributed to lower oil revenues, persistent capital expenditure overruns on mega-projects, and non-oil revenue risks if the prices returned to their under $70 per barrel. Public debt is expected to forecast to rise to 29.9% (official forecast) of GDP.

The government is increasingly turning to international debt markets for financing. As of March 2025, Saudi Arabia’s total public debt stood at SAR 1,328.8 trillion ($354.3 billion).

Saudi Arabia’s total public debt

As of March 2025

1,328.8

billion SAR

$354.3 billion

Domestic debt

797.1

billion SAR

$231.6 billion

billion SAR

External debt

$141.8 billion

(40.0% of total debt)

531.7

Despite these pressures, Saudi Arabia’s buffers remain robust (official reserve assets at US$ 454.29 billion as of March 2025 – six month high but slightly below September 2024)) and the country’s strong credit ratings provide room for further borrowing if needed. However, the pace and quality of fiscal reforms, along with the ability to diversify revenue sources and contain spending, will be critical in stabilizing the fiscal outlook and sustaining economic transformation in the face of ongoing oil market volatility and global uncertainties.

The budget deficit as % of GDP is projected at -2.3% of GDP for 2025, compared to 2.8% of GDP and 2% of GDP in 2024 and 2023, respectively.

If oil prices remain subdued in the coming months (despite its initial spike following the eruption of the Iran-Israel war) the kingdom’s fiscal deficit could widen to around 5% of GDP.

Saudi Arabia recorded a deficit of SAR 58.7 billion ($15.65 billion) in Q1 2025 – the largest quarterly shortfall since 2021 - driven by declining oil revenues and increased spending to support Vision 2030 development initiatives.

Total revenues reached SAR 263.62 billion, marking a 10.0% decline y/y, primarily due to a 18% y/y drop in oil revenues to SAR 150 billion in Q1 2025) – due to oil production reduction by the OPEC+ alliance, along with lower average crude oil prices relative to the same period in 2024.

Oil income accounted for 56% of total government revenues in Q1 2025, down from 62% in Q1 2024 – underscoring the vulnerability of fiscal balances to global oil market shifts.

Non-oil revenues continued to grow modestly, rising 2.% y/y to SAR 114.0 billion (with taxation on goods and services as the main contributor ) underpinned by structural economic reforms and the Kingdom’s diversification agenda under Vision 2030. Taxation on goods and services remained the largest contributor to non-oil income, generating SAR 71.56 billion (+2.37% y/y). However, this growth was insufficient to offset the decline in oil receipts.

Total government expenditures in Q1 2025 rose 5.0% y/y to SAR 322.3 billion, reflecting continued investment in strategic initiatives aligned with Vision 2030 goals and higher social spending – particularly on compensation of government employees and social benefits. Compensation for government employees remained the largest expenditure category at SAR 146.09 billion (+6.24% y/y), accounting for 45.3% of total spending.

Fiscal Sector

Saudi Arabia’s fiscal sector in early 2025 has come under renewed pressure as oil prices fell to four-year lows, averaging below $70 (end of May 2025 ) per barrel-well beneath the IMF’s estimated fiscal breakeven of over $90 per barrel.

In Q1 2025, the Kingdom posted a budget deficit of SAR 58.7 billion ($15.6 billion), the largest quarterly shortfall since 2021, as total revenues dropped 10% y/y to SAR 263.6 billion, driven by an 18%y/y plunge in oil revenues to SAR 149.8 billion.

Oil income accounted for just 56% of total government revenues in Q1 2025, down from 62% a year earlier, but underscoring the vulnerability of fiscal balances to global oil market shifts. In contrast, non-oil revenues continued to grow modestly, rising 2% y/y to SAR 114 billion, with taxation on goods and services as the main contributor. However, this growth was insufficient to offset the decline in oil receipts. Total government expenditures increased by 5.0% y/y to SAR 322.3 billion, reflecting continued investment in Vision 2030 projects and higher social spending, particularly on compensation for government employees and social benefits.

Executive Summary

At the end of Q1 2025, Saudi Arabia’s economy remains resilient but faces mounting external headwinds. Real GDP grew 2.7% y/y, supported by sustained non-oil sector expansion (+4.2% y/y) and strong consumer spending, even as oil GDP contracted before the start of the Israel-Iran war on June 13.

The rise in GDP in Q1 this year is a moderation from Q4 2024’s 4.48% surge. This deceleration was mainly due to a -1.4% y/y contraction in oil GDP, reflecting the impact of subdued oil prices (before the eruption of the Israel-Iran war), while non-oil GDP maintained sustained growth at 4.2% y/y – though moderating from 4.7% y/y in Q4 2024. Non-oil activities now account for 53.2% of total GDP.

Non-oil activities now account for over half of GDP, driven by Vision 2030 megaprojects, tourism, and digital transformation, while the labour market showed further improvement with overall unemployment at 3.5% and Saudi unemployment at 7.0% at the end of Q4 2024.

However, the fiscal position weakened: the Q1 2025 budget deficit widened to SAR 58.7 billion, as oil revenues fell 18% y/y, and spending on social programs and mega-projects remained high.

Non-oil exports surged 13.4% y/y in Q1 2025, but total exports declined 3.2% y/y as oil exports dropped sharply by 8.4% y/y, reducing oil’s share of total exports to 71.8% (from 75.9% in Q1 2024).

At the same time, imports rose 7.3% y/y, narrowing the trade surplus by March 2025. Inflation remains moderate at 2.1–2.3% (mainly driven by housing and food costs), but risks persist from elevated housing costs, potential subsidy reforms, and Red Sea shipping disruptions.

Looking ahead, GDP is projected to grow 3.6% in 2025, led by non-oil sector, but fiscal and external balances will remain sensitive to oil price volatility, global demand, and the pace of fiscal reforms. The outlook is cautiously optimistic: Vision 2030’s diversification is gaining traction, but sustaining momentum will require prudent fiscal management, accelerated private sector growth, and continued progress in non-oil exports, and job creation.

Non-oil sector growth in Q1 2025 was underpinned by dynamic consumer spending – in March 2025, consumer spending reached an all-time high of SAR 148 billion, up 17% y/y, while POS transactions rose 10% y/y and e-commerce soared 73.4% y/y (reflecting strong private consumption and retail momentum).

The labour market demonstrated further improvement. Overall unemployment fell to 3.5% in Q4 2024, from 3.7% in the previous quarter. Saudi unemployment fell to 7.0% in the same quarter, from 7.8% in the previous quarter (and from 8.4% in 2023), and female participation declined a bit to 36% in Q4 2024 from 36.2% in the previous quarter – despite this slight decline, the participation rate remains significantly higher than in previous years and reflects the ongoing progress of Saudi Arabia's labour market reforms.

Saudi Arabia’s industrial sector showed moderate but volatile growth in Q1 2025, with industrial production up 1.3% y/y in January, dipping 0.2% y/y in February due to weak oil output, and rebounded 2.0% y/y in March.

Manufacturing’s contribution in Saudi Arabia was uneven in early 2025. In January, output grew by 4.0% y/y, supported by gains in chemicals and refined petroleum products. Growth stagnated in February, rising just 0.2% y/y, as momentum in the sector softened despite continued increases in chemicals and food products.

In March, manufacturing output surged by 5.1% y/y, led by strong performances in chemicals (+14.3% y/y) and food products (+6.9% y/y). This pattern highlights both the sector’s growing importance to non-oil GDP and its vulnerability to global demand and supply chain risks.

Looking ahead, Saudi Arabia’s GDP is projected to grow 3.6% in 2025, with non-oil sectors forecast to expand by 4.5% and oil GDP by 2.7% - Saudi crude oil production is expected to average of 9.2 MMBD in FY2025.

Oil prices were expected to average $68.69/bbl in 2025 (our assumption), before the eruption of the Iran-Israel war. But with the onset with the serious military confrontation between both countries, Brent crude, the global benchmark, rose by 8% on June 13th, to $74 a barrel and the price per barrel could be around $90 if Israel hit key oil facilities in Iran, since the world would lose around 1.7m barrels per day from Iran.

The private sector remains optimistic, as reflected in a Purchasing Managers’ Index of 58.1 in March 2025. Sustaining the current trajectory will require accelerating high-impact sectors such as logistics and tourism, as well as addressing persistent labour market skill gaps to ensure the benefits of diversification are broadly shared amid ongoing global headwinds.

Fiscal Sector

Saudi Arabia’s fiscal sector in early 2025 has come under renewed pressure as oil prices fell to four-year lows, averaging below $70 (end of May 2025 ) per barrel-well beneath the IMF’s estimated fiscal breakeven of over $90 per barrel.

In Q1 2025, the Kingdom posted a budget deficit of SAR 58.7 billion ($15.6 billion), the largest quarterly shortfall since 2021, as total revenues dropped 10% y/y to SAR 263.6 billion, driven by an 18%y/y plunge in oil revenues to SAR 149.8 billion.

Oil income accounted for just 56% of total government revenues in Q1 2025, down from 62% a year earlier, but underscoring the vulnerability of fiscal balances to global oil market shifts. In contrast, non-oil revenues continued to grow modestly, rising 2% y/y to SAR 114 billion, with taxation on goods and services as the main contributor. However, this growth was insufficient to offset the decline in oil receipts. Total government expenditures increased by 5.0% y/y to SAR 322.3 billion, reflecting continued investment in Vision 2030 projects and higher social spending, particularly on compensation for government employees and social benefits.

The projected budget deficit for 2025 is SAR 101 billion, compared to an actual budget deficit of SAR 115.63 billion and SAR 80.95 billion in 2024 and 2023 respectively.

Looking ahead, the fiscal outlook for 2025 is challenging, with the deficit forecast to widen to 4.3% of GDP (SAR 188.77 billion) – above the government’s official projection of 2.3%. This wider gap is attributed to lower oil revenues, persistent capital expenditure overruns on mega-projects, and non-oil revenue risks if the prices returned to their under $70 per barrel. Public debt is expected to forecast to rise to 29.9% (official forecast) of GDP.

The government is increasingly turning to international debt markets for financing

Saudi Arabia’s total public debt

Despite these pressures, Saudi Arabia’s buffers remain robust (official reserve assets at US$ 454.29 billion as of March 2025 – six month high but slightly below September 2024)) and the country’s strong credit ratings provide room for further borrowing if needed. However, the pace and quality of fiscal reforms, along with the ability to diversify revenue sources and contain spending, will be critical in stabilizing the fiscal outlook and sustaining economic transformation in the face of ongoing oil market volatility and global uncertainties.

The budget deficit as % of GDP is projected at -2.3% of GDP for 2025, compared to 2.8% of GDP and 2% of GDP in 2024 and 2023, respectively.

If oil prices remain subdued in the coming months (despite its initial spike following the eruption of the Iran-Israel war) the kingdom’s fiscal deficit could widen to around 5% of GDP.

Saudi Arabia recorded a deficit of SAR 58.7 billion ($15.65 billion) in Q1 2025 – the largest quarterly shortfall since 2021 - driven by declining oil revenues and increased spending to support Vision 2030 development initiatives.

Total revenues reached SAR 263.62 billion, marking a 10.0% decline y/y, primarily due to a 18% y/y drop in oil revenues to SAR 150 billion in Q1 2025) – due to oil production reduction by the OPEC+ alliance, along with lower average crude oil prices relative to the same period in 2024.

Oil income accounted for 56% of total government revenues in Q1 2025, down from 62% in Q1 2024 – underscoring the vulnerability of fiscal balances to global oil market shifts.

Non-oil revenues continued to grow modestly, rising 2.% y/y to SAR 114.0 billion (with taxation on goods and services as the main contributor ) underpinned by structural economic reforms and the Kingdom’s diversification agenda under Vision 2030. Taxation on goods and services remained the largest contributor to non-oil income, generating SAR 71.56 billion (+2.37% y/y). However, this growth was insufficient to offset the decline in oil receipts.

Total government expenditures in Q1 2025 rose 5.0% y/y to SAR 322.3 billion, reflecting continued investment in strategic initiatives aligned with Vision 2030 goals and higher social spending – particularly on compensation of government employees and social benefits. Compensation for government employees remained the largest expenditure category at SAR 146.09 billion (+6.24% y/y), accounting for 45.3% of total spending.

As of March 2025

1,328.8

billion SAR

$354.3 billion

797.1

$231.6 billion

Domestic debt

billion SAR

billion SAR

External debt

$141.8 billion

(40.0% of total debt)

531.7

Oil Price Forecasts and Revenue Implications

(before June 13)

The sharp downward revision in oil price forecasts from multiple financial institutions presents a sobering fiscal reality:

-

The US Energy Information Administration (EIA) cut its 2025 Brent price forecast to $65.85 per barrel, down from $74.22 in its previous outlook.

-

JP Morgan reduced its 2025 Brent projection to $66 per barrel from $73.

-

Goldman Sachs anticipates year-end 2025 Brent prices at $62 per barrel.

These downward revisions stem from increased OPEC+ production, weaker global demand, subdued oil prices, and potential trade conflicts.

With oil revenue constituting 60.09% of government revenue in 2024, this oil price correction in early 2025 represents a significant fiscal shock. The government had anticipated a 3.7% decline in overall revenue in its 2025 budget, but current price trajectories suggest a much steeper revenue shortfall.

The US Energy Information Administration (EIA) cut its 2025 Brent price forecast to

$65.85

per barrel

down from

$74.22

in its previous outlook

JP Morgan reduced its 2025 Brent projection to

$66

per barrel

down from

in its previous outlook

$73

Goldman Sachs anticipates year-end 2025 Brent prices at

$62

per barrel

Monetary, Banking Sector performance

SAMA maintained its policy rate at 5.0% throughout Q1 2025, mirroring the Federal Reserve’s stance, while inflation grew by more than expected 2.3% y/y in March-driven mainly by housing rents (+11.9% y/y) and a moderate 2.0% rise in food prices. Persistent Red Sea disruptions, which have pushed up shipping costs, remain a potential imported inflation risk.

Saudi Arabia’s banking sector delivered outstanding performance in Q1 2025, with total bank credit reaching SAR 3.1 trillion ($827.2 billion) in March-a robust 16.26% y/y increase and the fastest growth in over three and a half years. This expansion was fuelled by a surge in corporate lending (accounted for 55.19% of total bank credit), which rose 22.3% y/y to SAR 1.71 trillion (reflecting strong demand from Vision 2030 projects). Asset quality remained exemplary, with the non-performing loan ratio at 1.3% (the lowest since 2016) – as of September 2024 and capital adequacy at 19.2% (as of September 2024), well above Basel III requirements.

The sector’s dynamism was further underscored by fintech innovation: mobile wallet transactions rose 45% y/y in 2024, and digital payments now (in 2024) accounting for 79% of all retail transactions.

Labour Market Outlook

Saudi unemployment for nationals fell to 6.3%, and female participation reached 36% in the same quarter, reflecting the impact of Vision 2030 reforms and Saudization policies. Nonetheless, youth unemployment still remains high highlighting ongoing skill mismatches despite private sector hiring of Saudi nationals (+5% growth in 2024) and ongoing reforms and economic diversification efforts.

The Purchasing Managers’employment sub-index in March 2025 points to continued job creation (hiring activity was at its fastest pace since Q3 2012), especially in construction and tourism, but the economy still relies on expatriate labour for many technical roles.

With 79% of employers planning to hire on a permanent basis, wage growth and nationalization efforts are expected to support labour market momentum, but the impact of large cuts in projects may slow hiring in the second half of the year.

The overall unemployment rate fell to 3.5% in 2024, compared to 4% in 2023 and over a 5-year period to 2024, it fell by a marked 3.9%. It stood at 7.4% in 2020.

Saudi unemployment rate fell to 6.3%. Over five years, it has fallen by 5.2% and stood at 12.6% in 2020.

Monetary, Banking Sector performance

SAMA maintained its policy rate at 5.0% throughout Q1 2025, mirroring the Federal Reserve’s stance, while inflation grew by more than expected 2.3% y/y in March-driven mainly by housing rents (+11.9% y/y) and a moderate 2.0% rise in food prices. Persistent Red Sea disruptions, which have pushed up shipping costs, remain a potential imported inflation risk.

Saudi Arabia’s banking sector delivered outstanding performance in Q1 2025, with total bank credit reaching SAR 3.1 trillion ($827.2 billion) in March-a robust 16.26% y/y increase and the fastest growth in over three and a half years. This expansion was fuelled by a surge in corporate lending (accounted for 55.19% of total bank credit), which rose 22.3% y/y to SAR 1.71 trillion (reflecting strong demand from Vision 2030 projects). Asset quality remained exemplary, with the non-performing loan ratio at 1.3% (the lowest since 2016) – as of September 2024 and capital adequacy at 19.2% (as of September 2024), well above Basel III requirements.

The sector’s dynamism was further underscored by fintech innovation: mobile wallet transactions rose 45% y/y in 2024, and digital payments now (in 2024) accounting for 79% of all retail transactions.

13.4%

80.7

billion SAR

30.6

billion SAR

y/y

to

and a record trade surplus in February

Imports are forecast at

901.7

billion SAR

(in 2025)

The External Sector

In Q1 2025, Saudi Arabia’s external sector showed both resilience and ongoing adjustment, as strong non-oil export growth (+13.4% y/y to SAR 80.7 billion) and a record trade surplus in February (SAR 30.6 billion) were offset by a sharp decline in oil exports and a rebound in imports by March (after a marked y/y decline in February) – resulting in a marked narrowing of the trade surplus to SAR 19.8 billion in the same month.

While non-oil exports—including a surge in re-exports—continued to gain ground and pushed the non-oil export-to-import ratio to 36.2% in Q1 2025, total exports fell 3.2% y/y and oil’s share of exports dropped to 71.8%. Imports rose 7.3% y/y in Q1, driven by machinery and transport equipment for Vision 2030 projects. These trends underscore both the progress and the vulnerabilities in Saudi Arabia’s external sector.

Oil export revenues are forecast at SAR 828 billion in 2025, slightly below 2024’s SAR 837.7 billion. Non-oil exports are projected to grow by 6% in 2025, reaching SAR 546 billion, a moderation from the record 13.1% growth in 2024 (SAR 515 billion) led by petrochemicals and tourism, but remain insufficient to offset oil revenue shortfalls. Imports are forecast at SAR 901.7 billion in 2025, a moderate 3.3% increase over 2024’s SAR 873 billion.

The trade balance is forecast at SAR 266.2 billion in 2025, only slightly lower than the SAR 272.6 billion surplus recorded in 2024. This stable but marginally reduced surplus is due to expectations of lower oil export revenues—pressured by both weaker prices and volumes—and prospects of modest import growth over 2025 – reflecting fiscal tightening and project reprioritization amid prospects of higher than projected fiscal deficit.

Risks to external sector include prolonged Red Sea disruptions, escalation of US-China trade-related frictions, China’s economic slowdown, and oil price volatility. However, the kingdom’s foreign exchange reserves (around $430 billion) continue to provide a substantial buffer.

While Foreign exchange reserves and prudent debt management (external debt: 40% of total) provide stability, accelerating diversification into Asian and African markets and enhancing logistics efficiency will be critical to mitigate external vulnerabilities and sustain Vision 2030 momentum.

3.3%

increase over 2024’s

(SAR 873 billion)

a moderate

Real GDP Growth

Saudi Arabia’s real GDP grew by 1.3% in 2024, after declining by 0.76% in 2023. In Q1 2025, it grew by 2.7% y/y, compared to 4.48% y/y in Q4 2024.

The Kingdom’s economy demonstrated moderate growth in Q1 2025, with real GDP expanding by 2.7% y/y – a significant slowdown from Q4 2024's 4.48% surge.

This deceleration stemmed primarily from oil GDP contracting by -1.4% y/y in Q1 (reversing Q4's 3.4% y/y growth).

Non-oil GDP remained resilient at 4.2% y/y growth in Q1, though slightly below Q4's 4.7% y/y pace. Prior to this, in 2024, the economy grew 1.3%, with non-oil activities expanding robustly by 4.3% - demonstrating strong structural momentum and domestic demand, even as oil activities contracted significantly - oil GDP contracted by 4.5% in 2024.

Non-oil sector contribution to GDP was 71.25% in Q3 2024, compared to 70.43% in Q2 2024 and 71.08% in Q1 2024.

On an annual basis, non-oil sector’s contribution rose to 68.39% in 2023, from 61.08% in 2022.

First

The non-oil sector continues to drive growth, mainly underpinned by strong consumer spending (17.3% y/y rise in March 2025 – all-time high to SAR 148 billion), indicating sustained private sector expansion, credit, construction and real estate sector growth.

The projected non-oil sector (4.5%) growth for 2025 may face downside risks, given recent potential spending cuts across various investment portfolios, which could constrain capital formation and dampen private sector activity in the second half of 2025.

Q1 2025 performance reveals four critical dynamics

Second

Oil sector volatility remains a structural challenge -- Q1's -1.4% decline shows the economy remains vulnerable to production policy shifts.

Third

The widening growth gap between non-oil and oil activities (4.2% vs -1.4%) underscores Vision 2030's progress but also highlights lingering fiscal vulnerabilities, as 60.09% of government revenue still comes from oil revenues (2024).

Fourth

The sustained non-oil growth momentum represents a critical validation of Vision 2030's structural reform agenda. However, the widening gap between oil and non-oil sector performance raises questions about long-term fiscal sustainability, as the non-oil sector remains indirectly dependent on oil-derived government spending for its continued expansion.

Consumption remained robust at the end of Q1 2025

In Q1 2025, Saudi Arabia experienced a robust surge in consumer spending, which rose by 17.3% y/y to SAR148 billion in March 2025.

This growth was mirrored in related indicators: point-of-sale transactions increased by 10% y/y, cash withdrawals grew by 8.2%, and e-commerce soared by 73.4% in March – reflecting strong private consumption and retail momentum.

The most significant gains were seen in jewellery (+77.3% y/y) and clothing & footwear (+38.1% y/y). Notably, this sharp increase in consumption occurred despite a challenging macroeconomic context.

Saudi consumers display a net positive spending outlook for 2025, in contrast to contractions seen in the US and Europe.

Purchasing Managers’ Index: Business Sentiment

The Riyad Bank Saudi Arabia Purchasing Managers’ Index registered 58.1 points in March 2025, reflecting continued robust expansion in the non-oil private sector, though moderating from 58.4 in February and a near 14-year high of 60.5 in January. (Anything above 50 points shows positive economic expansion).

The March 2025 figure, while indicating a slight cooling, remained well above the long-term average of 56.9, signalling sustained economic momentum.

The index performance reflects a controlled cooling, which may be beneficial for preventing overheating in specific sectors. The moderation in input costs and decline in output prices in March 2025 are particularly noteworthy despite robust consumer demand.

This provides a favourable environment for SAMA to maintain its current monetary stance without constraining real sector growth.

Industrial Production and Manufacturing

Overall Industrial Output

Saudi Arabia's industrial production index registered varied performance in early 2025:

Jan 2025

1.3%+

y/y

y/y

Jan 2025

4.0%+

Feb 2025

-0.2%

y/y

Feb 2025

+0.2%

y/y

Mar 2025

+2.0%

y/y

Mar 2025

+5.1%

y/y

Manufacturing Sector Performance

Saudi Arabia’s industrial sector in Q1 2025 displayed a pattern of moderate growth with some volatility. The year began with a 1.3% y/y increase in industrial production in January, signaling a modest recovery. February saw a brief contraction of 0.2% (the first decline since June 2024), largely due to persistent weakness in mining and quarrying - (especially oil extraction) i.e. driven primarily by a 0.7% y/y drop in mining and quarrying (reflecting lower oil output of 8.95 million bpd, down from 9.01 million bpd in February 2024), while manufacturing growth nearly stalled.

However, March marked a robust rebound, with industrial production rising 2.0% y/y , the fastest pace since December 2024. This was driven by a strong 5.1% surge in manufacturing, led by chemicals (+14.3%) and food products (+6.9%). This performance highlights the growing importance of the manufacturing sector in supporting non-oil GDP and advancing Saudi Arabia’s Vision 2030 economic diversification agenda.

However, while the manufacturing sector remains a cornerstone of Saudi Arabia’s non-oil economic diversification under Vision 2030, its contribution to growth in Q1 2025 was uneven. In January, manufacturing output grew by a solid 4.0% y/y, driven by increases in chemicals (+4.2% y/y) and refined petroleum products (+4.3% y/y). Manufacturing output then stagnated in February (+0.2% y/y), reflecting the sector’s vulnerability to external shocks such as supply chain disruptions and weaker demand from key markets like China, particularly for petrochemicals.

This muted performance limited manufacturing’s positive impact on non-oil GDP that month, even as chemicals (+3.5%) and food products (+6.3%) provided some support.

However, the sector rebounded strongly in March 2025 (as stated above), driven by robust growth in chemicals and food helping to offset continued weakness in mining and quarrying (oil).

This rebound underscores manufacturing’s potential as a key engine of non-oil momentum, but also highlights that its contribution can fluctuate significantly from month to month due to global demand and supply chain risks.

Policymakers should accelerate local content development programs to reduce import dependency and enhance manufacturing competitiveness, as the sector’s resilience is being tested by both external and domestic pressures.

Construction and Real Estate Sector

Saudi Arabia’s construction sector continued to underpin non-oil economic growth in Q1 2025, driven by Vision 2030 mega-projects, robust government spending, and strong demand in housing, infrastructure, and energy sectors.

The construction sector is forecast to grow by 4.4% in 2025, supported by a strong national budget totalling SAR1.3 trillion for 2025, which allocates significant resources to infrastructure and development.

This expansion is further reflected in a surge of new construction project licenses - in support of this expansion, the Saudi Ministry of Investment issued 3,800 construction licenses in 2024, signalling strong industry activity despite fiscal challenges.

Real estate prices recorded a 4.3% y/y increase in Q1 2025, with significant variations across segments:

Residential

+5.1%

y/y

Apartments

+1.2%

y/y

Agricultural

-1.1%

y/y

Villas

+10.3%

y/y

Commercial

+2.5%

y/y

Land plots

+5.3%

y/y

Shops and galleries

+5.1%

y/y

Bank lending to the real estate sector also remains robust. In March 2025, total bank credit in Saudi Arabia continued to grow robustly and reached SAR 3.1 trillion (USD 827.2 billion) – 16.26% y/y increase, from SAR 2.96 trillion at the end of 2024, with real estate activities accounting for 22% of corporate lending and growing by 40.5% y/y in March 2025 to reach SAR 374.5 billion.

This expansion reflects heightened demand for housing, commercial infrastructure, and development projects across the Kingdom’s mega-cities and giga-projects under Vision 2030. Bank lending to the real estate sector reached SAR 883 billion by the end of 2024, marking a 15.12% y/y rise - Real estate loans now account for 30% of total bank lending.

The construction and real estate sectors continue to be among the key drivers of Saudi Arabia’s non-oil economic growth.

The sharp rise in villa prices (+10.3%) highlights shifting post-pandemic housing preferences, while the more modest increase in apartment prices (+1.2%) suggests potential oversupply in urban markets. The decline in agricultural land values (-1.1%) points to ongoing challenges in agricultural profitability and water scarcity.

While the sector’s outlook remains positive, recent budget reprioritisations and reported spending slowdowns for non-strategic projects could create a two-tier market, with giga-projects progressing while mid-market developments face delays.

This fiscal consolidation reflects a strategic reprioritization of Vision 2030 initiatives. While high-profile international projects (2029 Asian Winter Games, Riyadh Expo 2030, FIFA World Cup 2034) remain protected, other Vision 2030 components will likely face delays or scaled-back implementation. The government faces a complex balancing act between fiscal prudence and maintaining economic momentum. The spending adjustments will need to be carefully calibrated to minimize negative impacts on the non-oil economy while addressing fiscal imbalances.

Fiscal Reserves and Buffers

Government reserves at the Saudi Central Bank (SAMA) expected to remain at SAR 390 billion through FY2025.

These reserves provide critical liquidity in the event of rising financing costs or deteriorating market access. The preservation of these reserves reflects prudent fiscal management and recognition of potential market volatility. However, the balance between utilizing reserves and increasing debt will be a crucial policy consideration if oil prices remain depressed through 2025.

Saudi Arabia will likely increase debt issuance substantially, potentially exceeding the record levels seen in 2024. The government's relatively low debt-to-GDP ratio and strong credit rating (recently upgraded to A+ by S&P) provide capacity for additional borrowing, though at potentially higher costs given global monetary conditions.

Saudi public debt is projected to rise to SAR 1,300 trillion in 2025 compared to SAR 1215.92 billion in 2024. In 2021 i.e. 5 years ago, it stood at SAR 938.01 billion – over this 5-year period, public debt is projected to rise by SAR 361.99 billion.

Public debt to GDP ratio (%) is projected to rise slightly to 29.9% of GDP in 2025, compared to 29.7% of GDP in 2024. In 2021, it stood at 28.8% of GDP. However, the public debt to GDP ratio of Saudi Arabia remains low by international standards.

SAMA Assets stood at SAR 1953.49 billion in March 2025 (rose by 5.08% y/y), compared to SAR 1,881.29 billion in December 2024 and SAR 1,859.01 billion in March 2024.

The steady rise in SAMA’s assets signals strengthening central bank reserves and improved liquidity in Saudi Arabia’s financial system over the past year. This upward trend enhances the Kingdom’s capacity to support monetary stability, manage external shocks, and maintain investor confidence amid ongoing fiscal and economic adjustments.

Reserve Assets stood at SAR 1,639.57 billion in 2024, compared to SAR 1,638.41 billion in 2023. At the end of Q1 2025, they stood at SAR 1703.6 billion. Reserve Assets/GDP ratio was 41.64% at the end of March 2025.

This upward trend signals improved external buffers and financial resilience, with reserves now accounting for 41.64% of GDP at the end of March 2025-well above global adequacy thresholds - helping the Kingdom maintain currency stability and confidence amid ongoing economic adjustments. Further, the increase in reserve assets enhances overall liquidity and financial resilience within the Saudi economy.

Inflation rose by only 1.7% in 2024, compared to 2.3% in 2024.

Despite the robust domestic demand and rents rising in excess of 10% (21% of the consumer price index, by far its main component), according to BNP Paribas, driven by sustained urbanisation and the growing working population, inflation remained under control in 2024.

Saudi Arabia’s annual inflation rate rose to 2.3% y/y in March 2025, up from 2.0% in February, and reaching its highest level since July 2023. This uptick slightly exceeded market forecasts of 2.2%.

Breakdown by Category (March 2025, y/y%):

On a monthly basis, consumer prices increased by 0.3% in March, following a 0.2% gain in February.

SAMA’s steady monetary policy stance, keeping rates at 5.0% since December 2024, reflects a cautious approach amid evolving inflationary pressures.

The March inflation uptick to 2.3% warrants close monitoring, as housing costs-particularly the 11.9% surge in apartment rents-are the primary driver. This likely reflects supply constraints in urban centres and growing demand from expatriate workers as Vision 2030 initiatives accelerate.

Housing, Water, Electricity, Gas, and Fuel

+6.9%, driven by housing rents (+8.2%) and particularly apartment rents (+11.9%).

Education

+1.1%, with higher education fees rising 4.3%.

Food & Beverages

+2.0%, with meat and poultry prices up 3.8%.

Restaurants & Hotels

+1.3%, driven by hotel services (+3.3%).

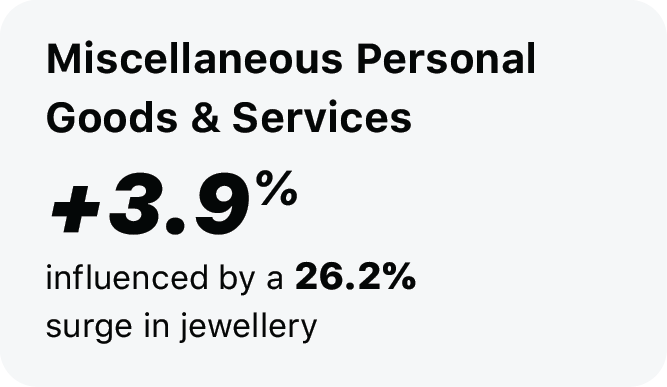

Miscellaneous Personal Goods & Services

+3.9%, influenced by a 26.2% surge in jewellery, watches, and valuable antiques.

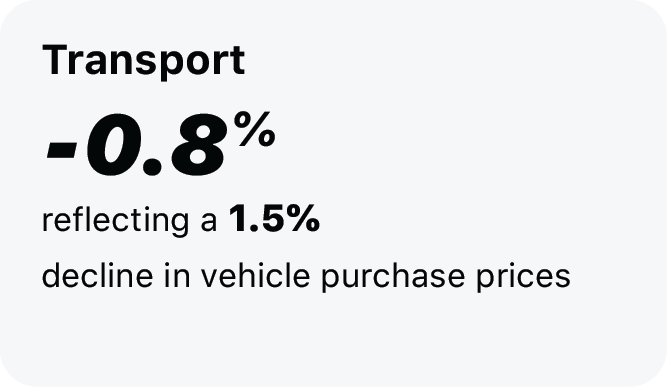

Transport

-0.8%, reflecting a 1.5% decline in vehicle purchase prices.

Entertainment & sports

+0.3%, up from -1.1% in February

Home Furnishings & Equipment

-2.6%, with furniture prices down 4.1%.

The banking and monetary sector performance

Strong credit growth: bank loans surged by 13.36% in 2024 to SAR 2855.35 billion, from SAR 2,518.79 billion in 2023.

Saudi Arabia's banking sector has demonstrated exceptional momentum; it’s banking sector continued its strong momentum in Q1 2025. Total bank credit reached SAR 3.1 trillion ($827.2 billion) in March 2025, marking a 16.26% y/y increase and the fastest growth in over 3.5 years. In February 2025, total bank credit stood at SAR 3.06 trillion, reflecting a 13.8% y/y increase and a 1.2% rise from January 2025. This y/y acceleration from February to March highlights robust lending activity, driven by strong demand for corporate loans and ongoing Vision 2030 projects.

Quarterly comparison:

Jan 2025

3.01

+15% y/y

+2% m/m

trillion SAR

Feb 2025

3.06

trillion SAR

+13.8% y/y

+1.2% m/m

Mar 2025

3.10

trillion SAR

+16.26% y/y

fastest in 3.5 years

This sustained growth in Q1 2025 underscores the sector’s resilience and its critical role in supporting Saudi Arabia’s economic transformation.

Key sectoral credit trends as of March 2025:

Corporate lending: accounted for 55.19% of total bank credit, up from 52.46% a year earlier i.e. y/y growth ; it grew by 22.3% y/y to exceed SAR 1.71 trillion. This surge is primarily driven by Vision 2030 project financing.

Real estate loans: accounted for 22% of business lending, grew by 40.5% y/y to SAR 374.5 billion.

Wholesale and retail trade: accounted for a 12.43% share, SAR 212.8 billion in lending.

Manufacturing: an 11.05% share, SAR 189.18 billion in lending.

Electricity, gas, and water supply: an 10.6% share, SAR 181.43 billion in lending.

Non-performing loan (NPL) ratio: 1.3% as of Q3 2024, the lowest since 2016.

Capital adequacy ratio: 19.4% in Q2 2024, well above the Basel III minimum of 10.5%.

Total bank assets: SAR 4.47 trillion in 2024, up from SAR 3.96 trillion in 2023 and surpassed the Financial Sector Development Program’s SAR 3.5 trillion target. In Q1 2025, bank assets rose further to SAR 4.71 trillion.

Capital Markets Development and Investment Landscape

Saudi Arabia's capital markets continue their remarkable development trajectory, with the Saudi Exchange (Tadawul) solidifying its position as the largest equity market in the Middle East and a key global player.

Tadawul’s market cap surged 463% over the past decade, reaching $2.7 trillion (SAR 10.1 trillion) by the end of 2024, making it the 9th largest global equity market and the largest emerging market outside Asia.

IPO Activity:

2024

42

Q1 2025

12

IPOs

IPOs

79%

5

on Tadawul

of GCC total

7

on Nomu

$4.1

raising

$1.8

generating

in proceeds

billion

billion

Notable listings

Um Al Qura for Development & Construction ($523 million) and Almoosa Health ($450 million)

2024: 42 IPOs (79% of GCC total), raising $4.1 billion.

Q1 2025: 12 IPOs (5 on Tadawul, 7 on Nomu), generating $1.8 billion in proceeds. Notable listings include Um Al Qura for Development & Construction ($523 million) and Almoosa Health ($450 million).

Foreign Investment: Foreign holdings reached 4.2% of total market cap (11% of free float) by end-2024, with Qualified Foreign Investor (QFI) participation steadily rising.

Tadawul’s Global Standing: Ranked 7th globally in IPO proceeds in 2024, with 91 IPOs raising $65 billion over the past decade.

Sukuk Issuance:

2024: Saudi issuers dominated MENA’s foreign-currency sukuk market, contributing significantly to regional volumes .

2025 Outlook: S&P Global forecasts $70–80 billion in foreign-currency sukuk issuance, driven by Saudi entities.

Yet, challenges persist: Low foreign participation (4.2% of market cap) compared to peers like the UAE (20%).

Concentration risk, with government-related entities constituting 64% of Tadawul’s market cap.

External Trade

From January to March 2025, Saudi Arabia’s external sector reflected both the challenges of oil market volatility and the clear momentum of its economic diversification agenda.

The Kingdom’s non-oil exports surged 13.4% y/y to SAR 80.7 billion ($21.6 billion) in Q1 2025, with national non-oil exports (excluding re-exports) up 9% and re-exports jumping 23.7%.

This robust growth in non-oil exports—led by chemicals (23.8% of non-oil exports, up 8.1%) and plastics/rubber (21.9% of non-oil exports, up 10.4%)—pushed the non-oil export-to-import ratio up to 36.2%, compared to 34.3% a year earlier.

Despite this progress, total merchandise exports fell 3.2% y/y in Q1 2025 to SAR 285.8 billion, as oil exports dropped 8.4% and their share of total exports declined from 75.9% to 71.8%.

Imports rose 7.3% y/y to SAR 222.7 billion, driven by strong demand for machinery, electrical equipment (26.6% of imports, up 18.7%), and transport equipment (14.6% of imports, up 17.3%)—all supporting major Vision 2030 projects. As a result, the merchandise trade surplus narrowed by 28% y/y to SAR 63.05 billion. China remained Saudi Arabia’s top trading partner for both exports (15.7% share) and imports (26.6% share).

A major development in early Q2 2025 is Saudi Aramco’s plan to boost crude oil exports to China to approximately 48 million barrels in May, up sharply from 35.5 million barrels in April. This surge follows Aramco’s new pricing strategy, with the official selling price for Arab Light crude cut by $2.30 per barrel for May deliveries, narrowing the premium over Oman-Dubai benchmarks to $1.20-the lowest in four months and near a four-year low.

These price cuts are a direct response to OPEC+’s decision to phase out production cuts and to defend market share in China amid a bearish oil market.

The sharp increase in Saudi crude allocations to China for May 2025 underscores the Kingdom’s reliance on Asian markets and its willingness to sacrifice per-barrel revenue for market share.

While this strategy may protect export volumes in the short term, it heightens Saudi Arabia’s exposure to demand fluctuations and economic slowdowns in China and the broader region, and policy shifts there.